At ZOOZ, we continuously strive to improve our products and enhance our offerings. The key is flexibility, variability, and optimization— and these three components go hand in hand to perfect payment stacks and optimize their performance. Here’s a quick recap of our latest feature upgrades:

New Product Features

New product features to extend your business possibilities. The latest additions include:

Webhook additions

Merchants are now able to resend the latest webhook-events for payments. This feature is paramount to making sure your system is up-to-date, regardless of communication stability. Learn more about webhooks here.

New Routing engine capabilities

Our smart routing engine is continuously enriched with new options for payment routing. Routing rules can then be adjusted to suit various business needs, changed in a heartbeat, and reflect the results almost instantly:

Alternative Payment Method (APM) routing— many merchants wish to increase their offering with new payment methods. APMs (Alternative (i.e., non-card)Payment Methods) have become a popular way to pay online. Merchants are now able to maximize the performance of such payments via the ZOOZ orchestration platform, with new routing options according to specific APMs. Please note that the rule's target provider will need to support the alternative payment method you’ve selected.

Card type: Routing according to card type is now also available via our orchestration platform.

What’s New? At ZOOZ, we continuously strive to improve our products and enhance our offerings. The key is flexibility, variability, and optimization— and these three components go hand in hand to perfect payment stacks and optimize their performance. Here’s a…

January 2021 marked the beginning of a new year and the official implementation of 3DS 2 guidelines for online transactions in Europe (the UK is due on 17 September 2021). 3DS 2 sparks concerns in merchants and providers alike. As…

To combat credit card fraud and protect consumers, card brands like MasterCard, Visa, American Express, Discover and JCB established the PCI Security Standards Council which mandates a set of security standards for managing online payments. What is PCI DSS?…

A well-designed payment stack is made to generate more money for your business. Who wouldn’t want that? But as it turns out, this concept is a bit more complex to implement in practice. As we’ve covered in recent articles, choosing a…

While COVID-19 has hit many sectors hard, e-commerce is one industry where business has boomed. With quarantines and social distancing limiting people’s ability to maintain their purchasing and spending habits in the physical world, consumers are forced to shop online….

Without noticing, COVID-19 has sped up the shift the entire payment ecosystem has been expecting for years— only instead of a slow and gradual transition, many sectors were forced to condense an otherwise year-long process into just a couple of…

Payment orchestration platforms have become the go-to solutions for businesses looking to optimize their payment performance. The following tips show how you can utilize ZOOZ’s unique solution-features to optimize the way you extract information, find payments, or make alterations to,…

The 3DS 2 Guide for Payment Professionals

By Dana Kemper, February 4, 2021

January 2021 marked the beginning of a new year and the official implementation of 3DS 2 guidelines for online transactions in Europe (the UK is due on 17 September 2021).

3DS 2 sparks concerns in merchants and providers alike. As with many new regulations/changes, the gaps between what’s desired and what exists are profound, and require time to adjust and align with all of the players involved in making this operation work. Let’s shed some light on what’s changed and what is required of you to comply.

The Then vs. The Now (3DS 1 vs. 3DS2)

While in the past 3DS was performed with the use of a OTP, The need to change 3DS grew in importance to reduce false declines and to improve the user experience while performing online payments.

What the EMVco* realized was that online fraud continues to expand, and thus requires better validation to ensure the security of transactions and customer identification. 3DS 1 also caused a drop in conversion rates, since cardholders had to undergo an unfriendly flow.

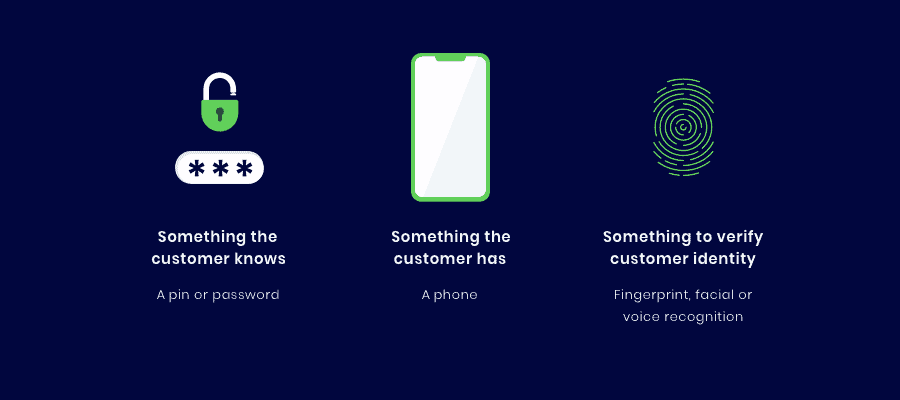

That’s when 3DS 2 was born. Designed around the principles of Strong Customer Authentication (SCA), the significant difference between 3DS 1 and 3DS 2 is that customer authentication should now be performed with at least two of the following identification methods: "something the user knows" (e.g., password), "something the user is" (e.g., fingerprint), "something the user owns" (e.g., mobile device).

The 3DS 2 flow corresponds with the data received from the actions the user performs in the device (such as fingerprint authentication, device ID, IP address, and more), and responds accordingly to finalize the user’s authentication.

As regulations came into effect in 01.01.2021, SCA is now mandatory for all online transactions in Europe— Card Issuers (Banks) in Europe are now obligated to use the above two-factor-authentication for all card payments. While there are some exemptions to the above (which we'll break down shortly), merchants are still advised not to rely on exemption-flows and calculate the most secure scenarios to ensure high approval rates.

The upside

While it may seem an obstacle at first, 3DS 2 has many benefits to both merchants and customers. Firstly, it allows payment providers to send more data to the cardholder’s issuing bank, e.g., device and order history. The bank can then use this data to recognize the customer for future purchases and prevent recurring requests for the user’s authentication. This has the potential to optimize the flow for buyers and create frictionless authentication for future purchases. 3DS 2 also gives buyers more flexible ways to authenticate their identities, e.g. via a thumbprint, app-based authentication, or a one-time password. Transactions that were authenticated will have a higher approval rate in the authorization step.

How does the new flow look like?

The flow begins when a buyer wishes to purchase an item/service. After inserting their card information, the merchant receives their request and enrolls them via the relevant 3DS flow.

Once the issuer receives a payment request, they review the contextual data in which it was made– the type of merchandise being purchased, the buyer’s shipping location, device type, etc.

At this point, the issuer may deem the information sufficient to approve the transaction. Otherwise, they may request the buyer to prove their identity with additional information.

While most transactions are frictionless - and occur without the buyer’s awareness - the issuer may occasionally request to perform a simple challenge to prove their identity. The issuer decides which challenge should be completed — a face recognition, a fingerprint, a one-time verification code, or else.

After the buyer provides the additional information, the issuer then reviews it and decides whether to approve/decline the transaction. The flow is now complete. Thanks to the additional information received, the issuer can rest assured of the buyer’s identity and accommodate their request.

The significant bits you need to know

3DS 2 is not free from potential downsides, primarily because it’s still in its formation state. Some gaps still exist between what’s desired and what exists in the field. For instance, banks are required to perform 2-step authentication flows, which means that a one-time passcode is insufficient and requires an additional step, e.g., confirmation via a bank application, fingerprint, face ID, etc. This turns out to be tricky, as even the most advanced banks—who have implemented the two-stage-verification— can still lose a hefty percentage of transactions due to 3DS.

Effect on customer experience

The new requirements may be foreign to many customers at first and can impact conversion rates and increase abandoned carts at checkout. Failure to complete payment flows can be either due to an unfamiliar authentication process or as a result of technical difficulties or broken flows at the backend. Our data analysis team recently discovered that many banks did not manage to implement all requirements such as responsive web design, two-factor authentication, and other technological conditions that significantly affect customer experience. Conversion rates due to these gaps have plummeted to 30%-40%.

Possible flows and exemptions

Exempting users from an SCA flow is useful since it increases the chance that the transaction will be frictionless (i.e., without an additional authentication step) and decreases the chances of user drop-outs. Suppose you are a merchant whose business model includes card-on-file like functionality or are processing one-click payments or recurring payments. In that case, you can enroll these payments via flows that are eligible for exemptions from 3DS. Bear in mind that the decision of whether to grant the exemption lies within the card issuer. Once they are exempted, the chargeback liability shifts back to you (as the merchant). Possible exemptions include:

A Transaction Risk Analysis (TRA) - This scenario can be implemented when a transaction is considered low risk. In that case, ZOOZ sends the authorization request to the issuer flagged as low risk (TRA flag). Be aware that the issuer may deny this claim and require strong authentication utilizing a Soft Decline response code.

Recurring Transactions and Merchant Initiated Transactions - Only the subscription or recurring cycle’s initial transaction or recurring cycle will require SCA. Subsequent charges will be exempted. A transaction is deemed "recurring" if it is for a fixed amount. In case the amount changes over time (such as when some utility bills are based on usage, like electricity, telecom services, car-sharing, etc.), such transactions will be called MIT (merchant initiated transaction) and will also be exempted. In both cases, the merchant must obtain the cardholder's consent for charging the card.

Soft decline - The card issuer always decides whether or not to honor the exemption. If strong customer authentication is deemed necessary by the issuer, the authorization will be declined using a specific reason code – Soft Decline.

Trusted beneficiaries - this exemption enables cardholders to add businesses they trust to a list of trusted beneficiaries to be held by the issuing bank. Once trusting a merchant, which is also termed as Merchant White Listing (MWL), cardholders can complete their electronic payments without the step-up authentication when shopping at that merchant in the future. Whitelisting merchants increase frictionless user experience and hence reduces cardholders’ shopping cart abandonment. You should be aware though, that merchants cannot white list themselves, and cardholders can remove merchants from their white list at any time. As required within GDPRregulations, the consent of a cardholder is needed to whitelist a merchant.

What we do to help with your compliance

The implementation of 3DS 2 and streamlining of procedures will take some time and further adjustments of all parties involved (issuers, banks, customers, and gateways alike). To equip you with the necessary tools and peace of mind, ZOOZ has set up to do the following:

As an orchestration platform, ZOOZ helps you monitor and spot decreases in acceptance rates due to 3DS. Thanks to the solution’s intuitive nature, you can easily change the configuration if you spot a drop according to your chosen parameters. Prevalent cases might be linked to a Bank’s choice of two-factor combination. Each bank decides independently of their product and compliance strategy in regards to SCA requirements.

Based on online transaction monitoring, we can optimize the conversion by routing 3DS authentication type for the better performing one (3DS 1 and 3DS 2) and communicate with Card Schemes and Issuing Banks to fix issues, improve process UX, and increase conversion rates.

Soft Decline - ZOOZ has two ways to manage Soft Decline: On behalf of the merchant, ZOOZ steps in and automatically initiates the authentication process using 3DS. The merchant is also able to handle Soft Declines via the PaymentsOS API. The decline reason code must be checked for each canceled order by retrieving the transaction details.

What lies ahead for 3DS 2

While records reveal that 22% of payments are lost when authenticated using 3D Secure, the reasons for this are rooted deep within the gaps in field-readiness. One of our customers has recently said that while “3DS 2 is the most discussed topic in the payment industry nowadays, yet we still witness many market gaps. While we view the implementation of 3DS 2 as a positive step and recognize its importance, real-time readiness is still lacking. So it’s up to us at this point to conduct thorough, ongoing checkups to ensure that transactions are processed smoothly”.

ZOOZ, as a payment orchestration platform, makes sure to support 3DS and related flows to give our customers the flexibility to change and supervise our customers’ payment flows to ensure that even in times of uncertainty, their payment processes are secure and optimized to the max.

Please check our Documentation for more information and drill down scenarios, implementation, and requirements to ensure your utmost compliance.

* EMVCo is collectively owned by American Express, Discover, JCB, MasterCard, UnionPay and Visa, and was formed in 1999 to enable the development and management of specifications to address the challenge of creating global interoperability and to deliver the adoption of secure technology to combat card fraud, while enabling innovation in the payments industry. More about EMVCo, here.

What’s New? At ZOOZ, we continuously strive to improve our products and enhance our offerings. The key is flexibility, variability, and optimization— and these three components go hand in hand to perfect payment stacks and optimize their performance. Here’s a…

January 2021 marked the beginning of a new year and the official implementation of 3DS 2 guidelines for online transactions in Europe (the UK is due on 17 September 2021). 3DS 2 sparks concerns in merchants and providers alike. As…

To combat credit card fraud and protect consumers, card brands like MasterCard, Visa, American Express, Discover and JCB established the PCI Security Standards Council which mandates a set of security standards for managing online payments. What is PCI DSS?…

A well-designed payment stack is made to generate more money for your business. Who wouldn’t want that? But as it turns out, this concept is a bit more complex to implement in practice. As we’ve covered in recent articles, choosing a…

While COVID-19 has hit many sectors hard, e-commerce is one industry where business has boomed. With quarantines and social distancing limiting people’s ability to maintain their purchasing and spending habits in the physical world, consumers are forced to shop online….

Without noticing, COVID-19 has sped up the shift the entire payment ecosystem has been expecting for years— only instead of a slow and gradual transition, many sectors were forced to condense an otherwise year-long process into just a couple of…

Payment orchestration platforms have become the go-to solutions for businesses looking to optimize their payment performance. The following tips show how you can utilize ZOOZ’s unique solution-features to optimize the way you extract information, find payments, or make alterations to,…

Tokenization: Everything you need to know

By Dana Kemper, December 23, 2020

To combat credit card fraud and protect consumers, card brands like MasterCard, Visa, American Express, Discover and JCB established the PCI Security Standards Council which mandates a set of security standards for managing online payments.

What is PCI DSS?

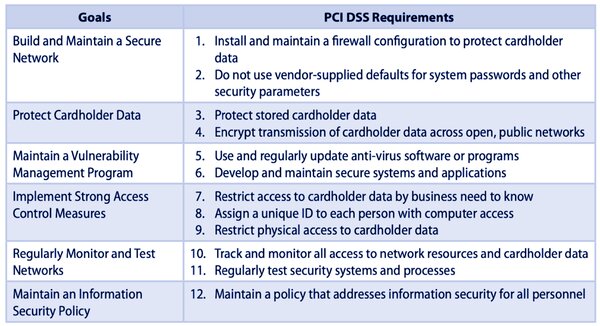

The Payment Card Industry Data Security Standard, better known as PCI DSS, is a global security standard for the acceptance and processing of credit cards. As you may already know, ensuring compliance with PCI Data Security Standards can be a challenging task. This is especially the case if your payment systems employ a patchwork of different services from different vendors. Just because the services you use are PCI compliant does not mean your operations will be considered so. PCI covers your entire cardholder data environment which not only includes the way you process payments and manage customer data but also how you connect those systems. According to the PCI Security Standards Council, PCI DSS: “covers technical and operational practices for system components included in or connected to environments with cardholder data.” It has 12 requirements designed to achieve 6 goals. These are outlined in the PCI Security Standards Council Reference Guide and copied below:

Do I need to be PCI compliant?

YES. If you process, store, or transmit credit card data, you're required to comply with this set of standards.

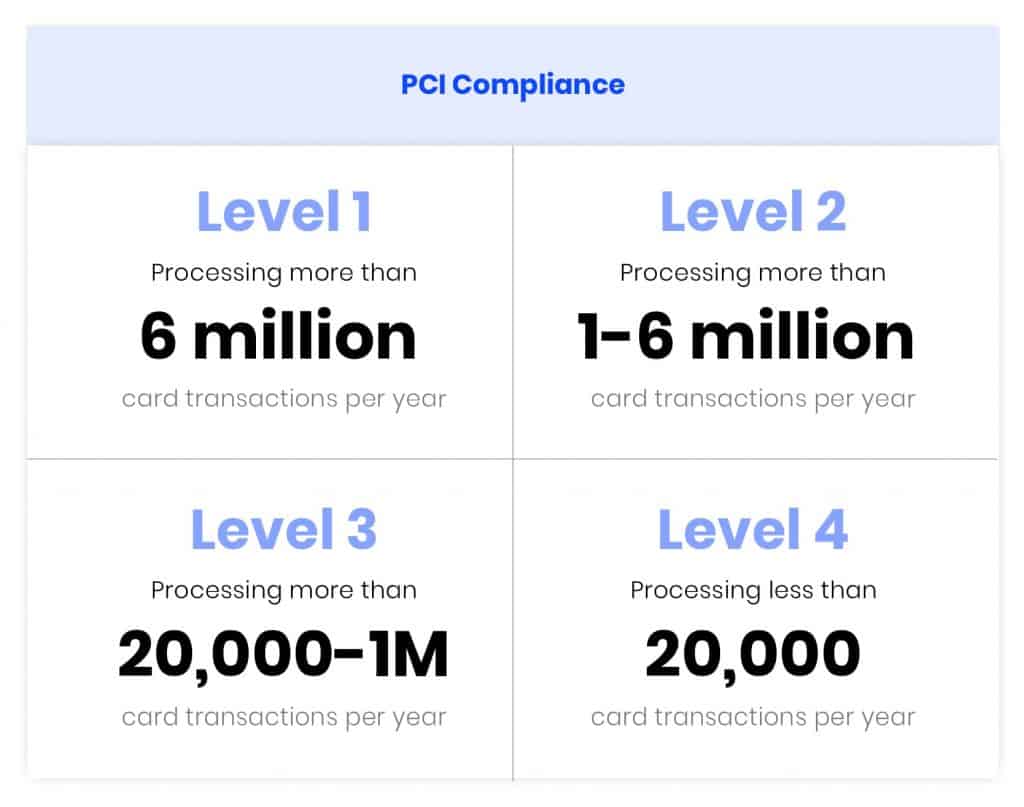

Levels of PCI compliance

Each card brand has its own set of compliance levels. Depending on the level you fall into, you’ll need to adhere to a specific set of requirements. And you'll need to ensure you are compliant with 100% of these requirements as failing even ONE element will result in non-compliance. To view the compliance levels set out by each card, see - Visa, Mastercard, Discover, American Express, & JCB.

If you accept multiple card brands, there's no need to panic. The major card companies have cooperated to make it easier. Visa, Mastercard, and Discover have the same criteria. If you also work with American Express or JCB in addition to these issuers, your merchant level will be the same as given to you by Visa, Mastercard, or Discover. Your compliance level will depend on the annual number of transactions.

PCI Compliance Levels

PCI Compliance Level 1

Processing more than 6 million card transactions per year.

PCI Compliance Level 2

Processing 1 to 6 million card transactions per year.

PCI Compliance Level 3

Processing 20,000 to 1 million card transactions per year.

PCI Compliance Level 4

Processing less than 20,000 card transactions per year.

How much does PCI compliance cost?

There’s no clear-cut answer to this question. It depends on the current business structures you have in place, and whether or not they require significant changes to conform to PCI standards. Larger-scale merchants with complex payment infrastructures and more employees will find the costs associated with becoming compliant much higher than smaller merchants with limited operations.

If you're a level 1 merchant with more than 6 million transactions per year, you'll need to have an onsite data security assessment by a Qualified Security Assessor (QSA). You will also need to set aside a budget to conduct regular vulnerability scanning, penetration testing, staff security training, and have dedicated resources to pay for security policy development. If you fall into level 2 and 3, audits by an external security expert might be required as well as staff training, vulnerability, and penetration testing. You'll also need to complete a Self-Assessment Questionnaire. Overall, the cost of compliance will always be lower than the cost of noncompliance. This is especially the case for larger merchants in a hyper-growth stage. Never mind the financial and reputational losses that stem from a data breach, you may be fined by card companies and lose the ability to accept credit cards altogether. That means your growth will come to an immediate halt. You may even risk going out of business!

What role does DSS tokenization play?

The PCI DSS requirements apply to all components that are in or connected to the cardholder data environment. This compromises of any person, process or technology that stores or transmits sensitive cardholder data. That's a lot of elements to cover!

One way to reduce your scope is to avoid storing and transmitting cardholder data altogether. That means not having any unencrypted credit card numbers, CVV or CVV2 or PIN numbers in your systems. That's where DSS tokenization comes in.

The Tokenization Process

DSS Tokenization helps to REDUCE not eliminate your scope. PCI Security Standards clearly state

Tokenization solutions do not eliminate the need to maintain and validate PCI DSS compliance, but they may simplify a merchant’s validation efforts by reducing the number of system components for which PCI DSS requirements apply.

Even if you've limited the existence of card details to the point of capture and the card data vault, ensured the data has no value to any potential criminal and made certain that adequate segregation exists between your platform and the card-holder data environment, you'll still need to comply with the PCI standards.

Reduce your scope with ZOOZ’s universal tokens

ZOOZ offers several ways of collecting and tokenizing a user's card details (javascript API, secure fields, token API), each requiring a different PCI scope. Universal tokens and PCI compliant token vault reduce your PCI compliance scope significantly by enabling you to avoid storing or transmitting raw credit card data in your systems. With reduced exposure to PCI data security compliance requirements, you'll save on compliance costs and sleep better at night in the knowledge that your operations are airtight when it comes to compliance. You'll also be able to offer your customers a more secure payments experience.

What’s New? At ZOOZ, we continuously strive to improve our products and enhance our offerings. The key is flexibility, variability, and optimization— and these three components go hand in hand to perfect payment stacks and optimize their performance. Here’s a…

January 2021 marked the beginning of a new year and the official implementation of 3DS 2 guidelines for online transactions in Europe (the UK is due on 17 September 2021). 3DS 2 sparks concerns in merchants and providers alike. As…

To combat credit card fraud and protect consumers, card brands like MasterCard, Visa, American Express, Discover and JCB established the PCI Security Standards Council which mandates a set of security standards for managing online payments. What is PCI DSS?…

A well-designed payment stack is made to generate more money for your business. Who wouldn’t want that? But as it turns out, this concept is a bit more complex to implement in practice. As we’ve covered in recent articles, choosing a…

While COVID-19 has hit many sectors hard, e-commerce is one industry where business has boomed. With quarantines and social distancing limiting people’s ability to maintain their purchasing and spending habits in the physical world, consumers are forced to shop online….

Without noticing, COVID-19 has sped up the shift the entire payment ecosystem has been expecting for years— only instead of a slow and gradual transition, many sectors were forced to condense an otherwise year-long process into just a couple of…

Payment orchestration platforms have become the go-to solutions for businesses looking to optimize their payment performance. The following tips show how you can utilize ZOOZ’s unique solution-features to optimize the way you extract information, find payments, or make alterations to,…

DIY: Build and optimize your payment stack with ease

By Dana Kemper, December 20, 2020

A well-designed payment stack is made to generate more money for your business. Who wouldn’t want that? But as it turns out, this concept is a bit more complex to implement in practice. As we’ve covered in recent articles, choosing a POL (payment orchestration layer) for your business is not as easy and straightforward as it may sound. First, the market is filled with different options, and while some overlapping exists between solutions, they still differ from each other and there’s not a single solution that can offer a one-stop-shop experience. On top of that, there’s the ongoing division between open vs. closed payment solutions, each with their characteristics and pros and cons, which make the decision-making even more complex. Is there a middle way? Can you get a top-notch optimization mechanism (associated with open payment solutions) with the simplicity which usually defines closed payment solutions? and moreover - can you actually do it by yourself?

Open vs. Closed

It’s important to stop for a moment and redefine what open and closed payment solutions are. At their simplest, open solutions allow you - the merchant - to have full control on how you route your payments and to which payment provider(s). Closed solutions won’t allow you to have that freedom of choice, but they will take the responsibility off of you by making automated routing decisions according to their own logic/algorithms. It is, therefore, a battle between tailored payment routing (with maximum payment optimization) of open solutions vs. the ‘plug-and-play’ benefit of closed solutions.

The key components of optimization

Optimization is a process of maximizing performance and generating the highest output by investing the smallest input (e.g. minimal man-hours, money, or a combination of the two). In the payment world, optimization becomes an essential key for growth and to maximize a business's ROI. We see the following four components as important catalysts to payment optimization:

High approval rates (i.e. more successful payments)

How to get there

Improved customer experience

Customer experience and satisfaction are important factors that help to reduce cart abandonment and make sure payments are finalized once the user gets to the checkout process. This is an elusive process that often ends in cart abandonment. Merchants need to do everything in their power to maximize the probability of payment fulfilment. To do that, they need to offer their customers multiple payment options to pay with, a secure, easy and straightforward interface, and added tools on their side (the merchant’s) to increase the probability that transactions will be authorized (more on that is coming up next).

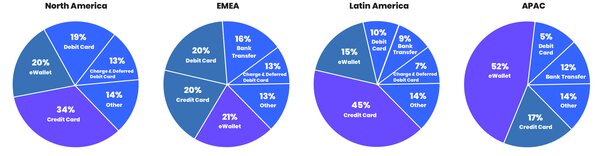

Data-based decision making

Payment routing and optimization should be done smartly. Payments differ in geographical areas, methods (credit cards, eWallets, etc.) and additional factors, which affect the probability of certain payments to be more or less successful when sent via one PSP or another. Optimization is achieved by tweaking and making changes to an existing stack according to its ongoing performance. So solutions need to enable data extraction to allow merchants to change their payment stack accordingly - i.e. to reflect the data. The chart below shows the a general division of the recorded use of payment methods in 2019. The rise in the use of eWallets is definitly a force to be reckoned with. Merchants need to be on top of their game and be aware of changes in payment trends etc.

Every business aims to eventually invest as little resources as possible while getting the best ROI in return. So a payment solution should be easy to operate (without added development), and has to reflect the results of the actions performed in it immediately. Check the video below demonstrating how easy rule-setting can be. Merchants can continuously tweak and optimize their rule-logic according to the data and reports they receive from the system. The easy rule-setting mechanism requires only minimal technical knowledge and allows payment teams to immediately make changes to reflect the results they see in real-time.

High approval rates

Approval rates are affected by multiple factors - sometimes it’s a matter of one PSP that has a better transaction approval rate in certain locations or with certain payment methods, while sometimes transactions can be flagged as fraudulent (whether they are indeed fraudulent or not). To eliminate or reduce these difficulties, merchants can devise their routing rules according to their business logic. To reduce unnecessary fraud flagging, merchants need to comply with PSD2 and other mandates so that they could verify the buyer beforehand. This is also something that a POL can help with, as POLs need to comply with regulations as well.

How POPs help you to optimize

All of the four components we’ve mentioned above should be implementable and streamlined via one place - and that’s where POLs come in. Many businesses wish to avoid - and very rightfully so - the need to add more work and programming on their side to such solutions. Often-times, the payment personal doesn't have an engineering background and since they are the main users of these solutions, the solutions should be a perfect fit for their needs and easy to operate.

We’ve mentioned before the classifications of payment solutions to closed and open. Many businesses opt for closed solutions because they are seemingly easier to operate and fuss-free. The caveat is again the lack of manual optimization options so the results are sub-optimal to what they can and should aim to. Open solutions might require more attention, but they offer far greater optimization options, which in the greater scope of things, can serve your business objectives much better.

Easy optimization, DIY style

Is there a middle way? Can you overcome complexity and the need to invest many man-hours of development and monitoring and still get a perfectly customizable solution to give you the utmost optimization?

The answer is yes - some solutions do offer a very straightforward platforms that eliminates the complexity and at the same time allows you to control and devise your business rules quickly and efficiently - without the need to invest further money and man-hours in development. That way, you can benefit from the control and adaptability of an open solution with an ease which is usually associated with closed solutions. At ZOOZ, that was (and still is) one of our core guidelines when we designed our solution: simplicity, greater control and adaptability. Specifically designed for payment teams, the solutions is both extremely straightforward and self-explanatory, while at the same time offers very high-end capabilities of routing, data-analyzing and optimization. You can dive in and open a quick (and free) demo account to get the look and feel of our solution for yourself. As mentioned above, the core pillars of optimization in payments usually revolve around customer experience, data-based decision making, efficiency and high approval rates. Eventually - and due to the nature of the payment ecosystem - solutions need to be flexible enough to allow tweaks and changes to support these core pillars. Optimization therefore is very much associated with the DIY approach of open payment platforms, and that should be taken into account when devising a payment strategy. Eventually optimization requires control from your side, and cannot be done without a certain amount of supervision, but that also doesn't mean that controlling your own system should be overly complicated.

Stay informed with all of the latest industry news and updates by signing up for our newsletter.

What’s New? At ZOOZ, we continuously strive to improve our products and enhance our offerings. The key is flexibility, variability, and optimization— and these three components go hand in hand to perfect payment stacks and optimize their performance. Here’s a…

January 2021 marked the beginning of a new year and the official implementation of 3DS 2 guidelines for online transactions in Europe (the UK is due on 17 September 2021). 3DS 2 sparks concerns in merchants and providers alike. As…

To combat credit card fraud and protect consumers, card brands like MasterCard, Visa, American Express, Discover and JCB established the PCI Security Standards Council which mandates a set of security standards for managing online payments. What is PCI DSS?…

A well-designed payment stack is made to generate more money for your business. Who wouldn’t want that? But as it turns out, this concept is a bit more complex to implement in practice. As we’ve covered in recent articles, choosing a…

While COVID-19 has hit many sectors hard, e-commerce is one industry where business has boomed. With quarantines and social distancing limiting people’s ability to maintain their purchasing and spending habits in the physical world, consumers are forced to shop online….

Without noticing, COVID-19 has sped up the shift the entire payment ecosystem has been expecting for years— only instead of a slow and gradual transition, many sectors were forced to condense an otherwise year-long process into just a couple of…

Payment orchestration platforms have become the go-to solutions for businesses looking to optimize their payment performance. The following tips show how you can utilize ZOOZ’s unique solution-features to optimize the way you extract information, find payments, or make alterations to,…

COVID-19 e-commerce trends that are here to stay

By Dana Kemper, November 22, 2020

While COVID-19 has hit many sectors hard, e-commerce is one industry where business has boomed. With quarantines and social distancing limiting people’s ability to maintain their purchasing and spending habits in the physical world, consumers are forced to shop online. Businesses are also having to respond to new, constantly changing guidelines that require modifying the services and products they have on offer. Here's the lowdown on some of the main COVID-19-driven e-commerce consumer trends that are far from disappearing:

Social purchasing

With people unable to gather in the streets, they have been gathering on social media. An April study that surveyed over 25,000 consumers shows that social media engagement increased by 61% during COVID-19 social distancing. According to the study, overall facebook usage has increased 37%. The increase has been most considerable in the 18-34 age group, with a 40% or above usage spike on Facebook and Instagram. Chinese social media has also seen a dramatic rise in use, with a 58% increase on the social media apps Wechat and Weibo.

This increased engagement in social media has translated into more online sales. Instagram reported a 76% spike in engagement on #ad posts, as well as a 22% rise in Instagram campaign impressions from Q4 2019 to Q1 2020.

In May 2020, Facebook and Instagram took e-commerce integrations on social media one step further. Both of these social media giants rolled out Shops (Facebook, Instagram), a service that allows Facebookers and Instagrammers to buy products and purchase services right from a business’s Facebook page or Instagram profile. Instagram describes Shops as a native shopping experience, “an immersive fullscreen storefront that enables businesses to build their brand story and drive product discovery”. Facebook CEO Mark Zuckerberg described Shops as a way to support businesses whose business suffered in the wake of COVID-19, although, he adds, he sees this trend continuing to climb even once we put COVID-19 behind us. “I do think we’re going to continue living more of our lives online and doing more business online.”

Online donations

The for-profit sector is not the only market segment that’s taken a hit during COVID-19. Social distancing made it impossible to arrange physical fundraisers, or collect donations door-to-door. The income sources of musicians and other performers were hurt in particular, as concerts, tours and festivals were cancelled. Physical fitness professionals such as personal trainers and sports instructors also suffered at the hand of social distancing. These past few months have seen artists, trainers, and other businesses increase requests for donations online, via online payment services. Companies who provide infrastructure for these artists and small businesses have been supportive in accommodating these requests.

Just like social purchasing, online donations, of course, have existed before the onset of the pandemic. Amazon Smile is an established service that allows shoppers to donate half a percent of the amount of certain purchases to charity. Founded in 2013, Patreon is a subscription-based service that allows fans to make weekly payments to support creators they love. Awareness of online donation practices have existed for a while, but COVID-19 has given them a significant boost.

In April, Spotify launched Artist Fundraising Pick. Spotify artists can now add a donate button to their Spotify profile. Artists can choose to collect donations for their own work, or on behalf of a charity. In May, Spotify reported that “thousands of fans have already supported 10,000 artists through Cash App,” and that donations reached one million dollars. In addition to Cash App, artists can collect donations via PayPal and GoFundMe. Soundcloud is another major music platform that launched a donation button in April, allowing musicians to collect donations via Kickstarter, Bandcamp, Patreon and Paypal.

Fitness businesses and individuals are jumping on the donation wagon, too. ClassPass, a giant online workout platform, has set up a donation service that allows users to donate to their favorite trainers and studios. Love Sweat Fitness, a popular wellness platform, is also requesting donations for open-to-all zoom events. Individual trainers affected by COVID-19 social distancing have also incorporated donation buttons on various social media sites. Liz Crosby, a popular Instagram yoga teacher, is requesting donations for YouTube lessons via Venmo or PayPal.

Squarespace, who hosts over 2 million live websites, posted a list of COVID-19 resources for its customers, including instructions on how to incorporate a donate button into their website.

Veteran “buy now, pay later” (BNPL) payment services are seeing a spike in use. Klarna a BNPL service founded in 2005, has seen an 18% spike in apparel, footwear and accessory purchases among Gen Zers (ages 18–23). In one week in April, Klarna app users’ share of spending on home and garden items grew by 26% among Gen Zers. Klarna reports an overall increase in usage. “The number of daily active users peaked at the beginning of April and reached the all-time high so far this year,” Klarna said. Paypal, who also offers “buy now, pay later” in the form of PayPal Credit, also seems to be on a good path to weathering the pandemic with its assets intact, or strengthened.

Klarna and PayPal aren’t the only BNPL services who benefited from COVID-19. Other BNPL services report an increase in their average order value, or AVO. An April 30 article cites an AVO increase of 85% for Affirm, a San-Francisco-based APNL company. Australian-based BNPL AfterPay boasts a whopping 1M new users due to the COVID-19 pandemic. Reportedly, the platform attracted “over 15 million app and site visits,” and “its retail partners got nearly 10 million lead referrals from visitors to Afterpay’s Shop Directory. These numbers put Afterpay among the fastest-growing eCommerce payment companies on the market.” According to AfterPay, there are upward of 15,000 brands and merchants that either offer Afterpay or are in the process of joining its services. These brands include, among others, American Eagle, Birkenstock, and Marc Jacobs Beauty.

SplitIt, another APNL credit app who saw a 20% AVO increase, is calling out to businesses to adjust their payment offerings in the wake of COVID-19. In a June Facebook post, The New York-based company wrote that “24% of consumers do not expect to return to shopping malls for more than six months following post-covid-19 reopenings”. Because spending habits are changing, they say, there is a “rising demand to spread costs via interest-free instalments. Online retailers need to revisit their product portfolios to include payment options that are reflective of this new buying culture.”

Even Apple has joined the Buy Now, Pay Later revolution, launching the Apple Card Monthly Installment Plan in June. The plan allows consumers to receive an iPhone immediately, paying off the product’s full amount over several interest-free installments.

Brick-and-mortar converts to online

Ask anyone with access to electricity and an internet connection, and they’ll be able to cite at least one example of a brick-and-mortar business that was pushed online during the pandemic. Physical stores saw drops in store visits as steep as 90% in one month. In the early days of COVID-19 social distancing, the grocery and food sectors were most significantly affected. 14% of shoppers in one poll reported that they started shopping for groceries online due to social distancing. The difference between 2019 and 2020 in terms of online vs. offline sales is striking: one source reports that eCommerce sales accounted for a whopping 30% of total retail sales in the US in 2020, as opposed to 11% in 2019.

Shipbob, an e-commerce fulfilment solution company, aggregates data from over 3,000 merchants who “collectively ship out millions of items every month” via the company’s fulfilment center. On June 11, Shipbob reported rolling month-to-month unit volume increases in the following categories:

Nutrition: 49% increase

Beauty: 48% increase

Apparel and accessories: 96% increase

Food and beverage: 16% increase

Electronics: 25% increase

Toys and games: 44% increase

Household goods: 72% increase

Jewelry: 13% increase

Who are the businesses behind these increased online sales? Food delivery companies are one notable example, with restaurants being closed for sit-and-eat services due to social distancing. According to Second Measure, a company that analyzes billions of purchases, as of the end of April, meal delivery service sales nearly doubled year-over-year. People magazine compiled a list of restaurants that deliver nationally in the US, in honor of the COVID-19 epidemic. These include New York City’s iconic Milkbar, Lou Malnati’s Chicago deep dish pizza restaurant.

Innovation and diversification

There is no question that the COVID-19 pandemic has created a new reality. For some, social distancing has necessitated a change in socialization habits. For most, the virus floated health concerns to the top of the priority list. For many businesses, the pandemic meant that they had to change modes of operation, or risk going under. According to CBS news, 722 US companies sought bankruptcy protection in March and April, a 48% increase for the same period of the previous year. Large companies that succumbed to bankruptcy during this period included Hertz, J. Crew, J.C. Penney and Neiman Marcus. But other companies have managed to keep their head above water by innovating and diversifying.

Wolt, a Finnish food delivery service that operates in 22 markets, took advantage of its delivery infrastructure to deliver beauty products on top of its existing restaurant meal offerings. Wolt subsequently partnered with grocery stores and pharmacies to offer deliveries from these businesses as well, and was able to substantially grow their online payment business.

Nextdoor, a California-based neighborhood social networking app founded in 2011, saw an 80% month-over-month increase in daily engagement. Nextdoor was able to respond in a timely and sensitive manner to COVID-19 needs such as supporting struggling local businesses and providing aid to health care workers. A Google Marketing report explains that Nextdoor created new features to address specific pandemic-related needs, but made core features easily discoverable to draw in users and retain them. Help Maps is one such feature; it allows users to indicate when they’re available to help a neighbour in need.

Businesses in other sectors have been ingenious in responding to the pandemic’s needs of the moment. Alcohol sales in Switzerland dropped by up to 25%; in Ireland, a drop of 35% was recorded in April 2020, compared to April 2019. US alcohol sales were also affected. Distilleries across the globe responded to the changing fiscal and health reality by producing alcohol-based hand sanitizer. One website lists over 800 distilleries in the United States alone that are producing hand sanitizer. Many of these distilleries sell both hand sanitizer and their core product, spirits, online.

Other sectors have shown endless creativity in responding to the pandemic. Airlines turn from transporting people to transporting cargo, with some airlines removing seats from their aircraft to create seatless jets. Huge companies like Ford and General Motors are manufacturing Personal Protection Equipment such as masks and protective clothing.

An Online Revolution

Whereas physical retail took a huge hit during the pandemic, e-commerce has benefitted from a broad spectrum of exciting opportunities. Businesses that had only existed offline have capitalized on the accessibility and simplicity of online shopping. Simultaneously, businesses that previously thrived online are doing even better, and the future looks good. A study of over 1,000 consumers predicts that by the end of 2020, market penetration for online grocery shopping will be 12%. Companies that have undergone a digital payment transformation, migrating to e-commerce or expanding their digital offerings, have no reason to go back; experts are optimistic that these trends are here to stay.

What’s New? At ZOOZ, we continuously strive to improve our products and enhance our offerings. The key is flexibility, variability, and optimization— and these three components go hand in hand to perfect payment stacks and optimize their performance. Here’s a…

January 2021 marked the beginning of a new year and the official implementation of 3DS 2 guidelines for online transactions in Europe (the UK is due on 17 September 2021). 3DS 2 sparks concerns in merchants and providers alike. As…

To combat credit card fraud and protect consumers, card brands like MasterCard, Visa, American Express, Discover and JCB established the PCI Security Standards Council which mandates a set of security standards for managing online payments. What is PCI DSS?…

A well-designed payment stack is made to generate more money for your business. Who wouldn’t want that? But as it turns out, this concept is a bit more complex to implement in practice. As we’ve covered in recent articles, choosing a…

While COVID-19 has hit many sectors hard, e-commerce is one industry where business has boomed. With quarantines and social distancing limiting people’s ability to maintain their purchasing and spending habits in the physical world, consumers are forced to shop online….

Without noticing, COVID-19 has sped up the shift the entire payment ecosystem has been expecting for years— only instead of a slow and gradual transition, many sectors were forced to condense an otherwise year-long process into just a couple of…

Payment orchestration platforms have become the go-to solutions for businesses looking to optimize their payment performance. The following tips show how you can utilize ZOOZ’s unique solution-features to optimize the way you extract information, find payments, or make alterations to,…

Trends of change in E-commerce: new reality supported by data

By Dana Kemper, November 15, 2020

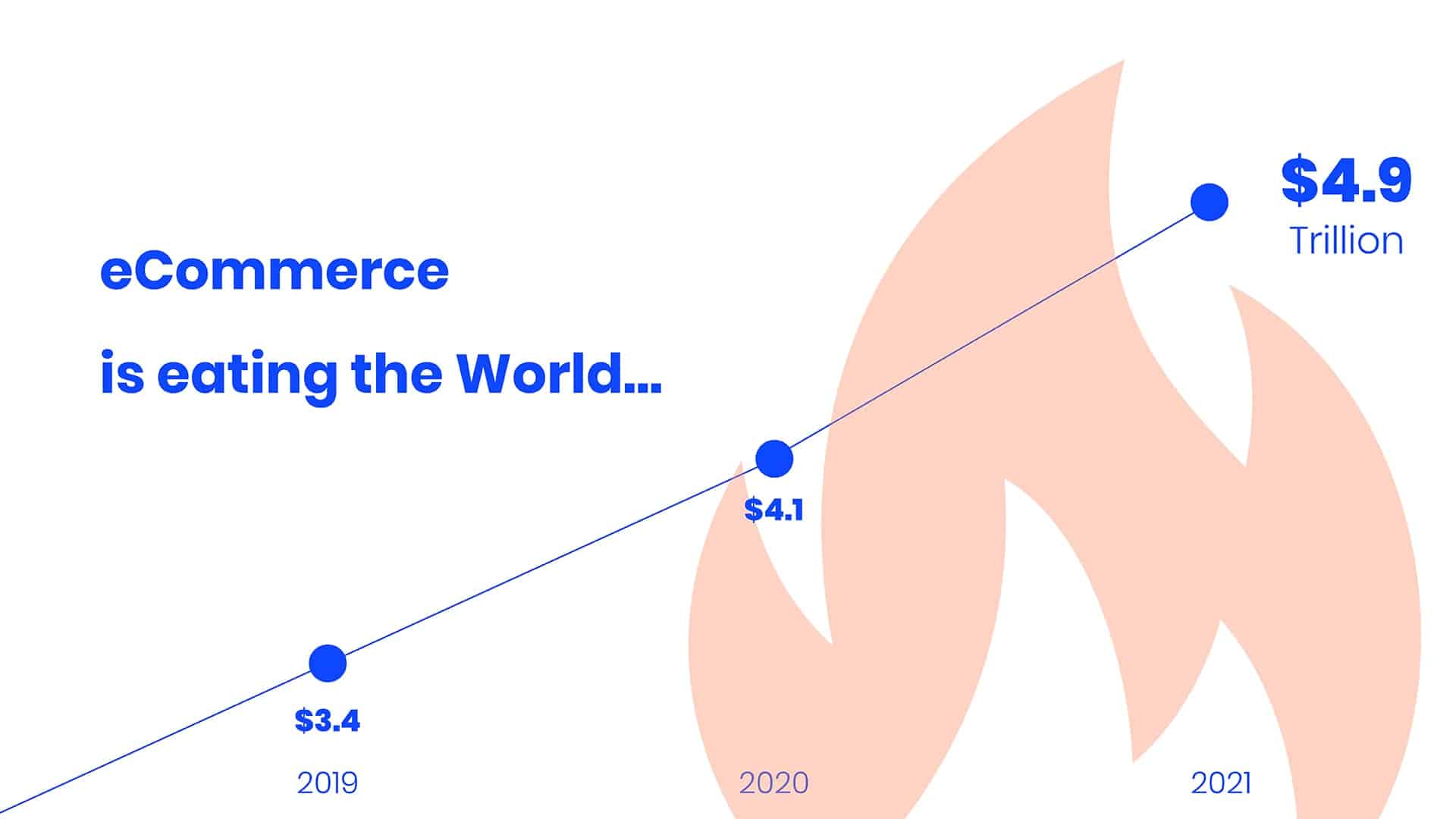

Without noticing, COVID-19 has sped up the shift the entire payment ecosystem has been expecting for years— only instead of a slow and gradual transition, many sectors were forced to condense an otherwise year-long process into just a couple of months. The surge in online commerce, contactless payment methods, digital wallets, and BNPL (buy-now-pay-later) schemes are the best representations of this changing landscape.

The new model of E-commerce is also unique in nature—not just speed. It reflects a very specific reality shaped by Covid-19; A newfound home-centric sphere that drives away most aspects of outdoor-leisure and travel, while simultaneously accelerating all things consumers can utilize indoors.

E-Commerce growth overtime January-November 2020

Trends reversed

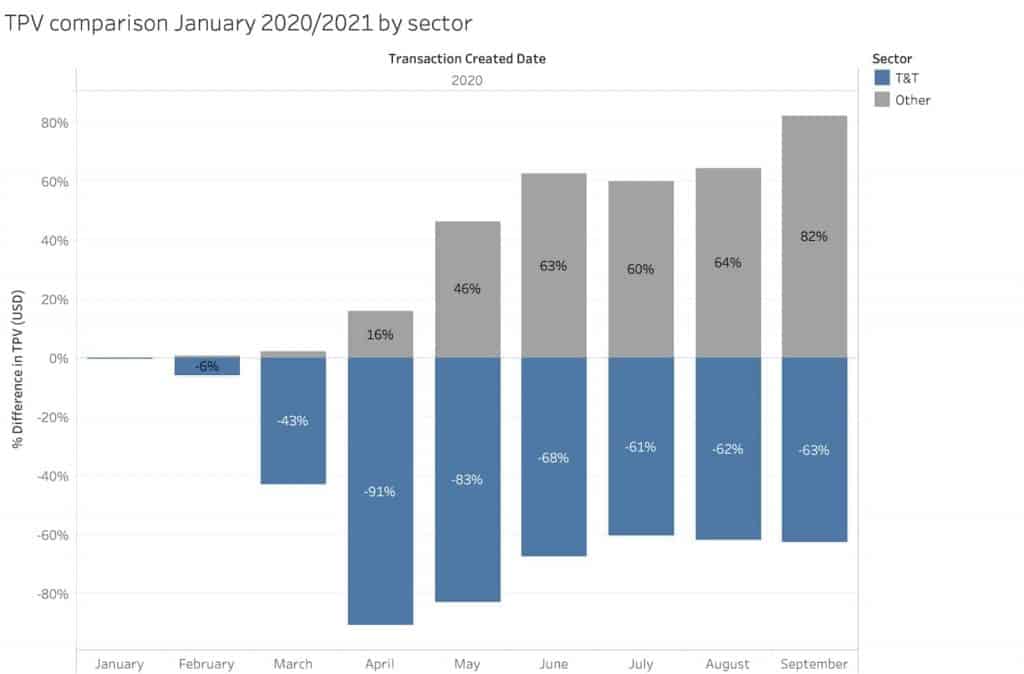

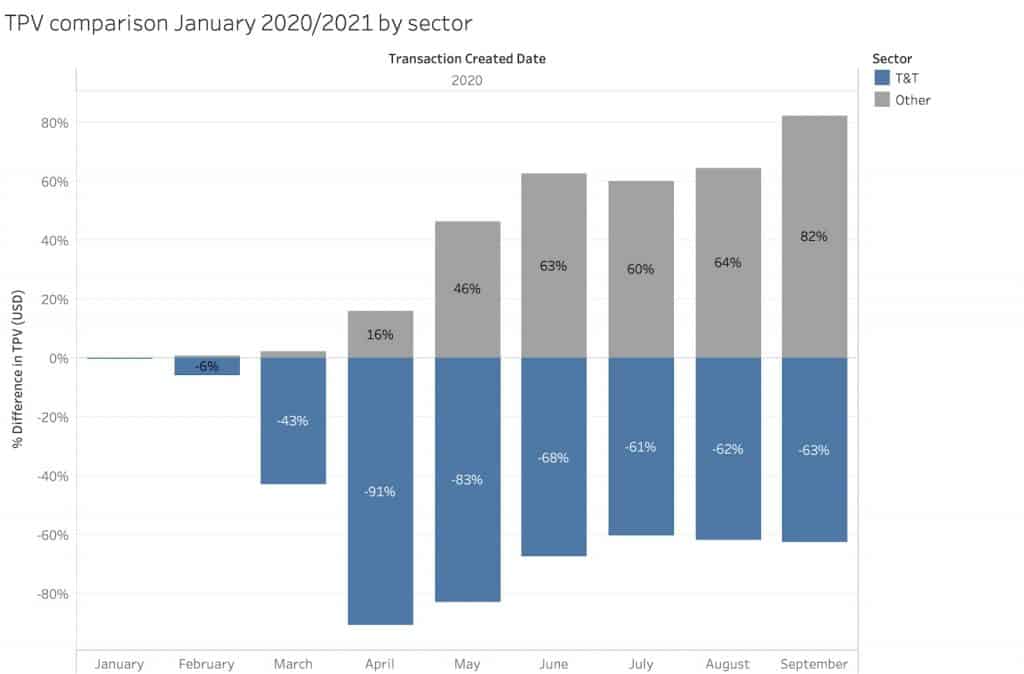

As consumers focus more on home-commerce, we witness how the scope of travel and transportation switch places with other sectors like apparel, leisure (that is non-outdoor-dependent), and more. This is all logical considering the new reality, but it is pretty staggering to see a trend pretty much turn around in mere several months. The graph below shows the gradual shift over the course of 8 months, from January 2020 to September 2020 (*T&T stands for Travel & Transport):

Does geography affect the rate of E-commerce penetration?

The answer is both yes and no.

Our data shows that E-commerce has grown on a global scale, i.e. it has been experiencing a big increase everywhere, and across all regions.

The relative jump is what makes the difference and emphasizes the gap between developing and developed countries, and a main aspect to this is their starting point and the relative jump they had to perform.

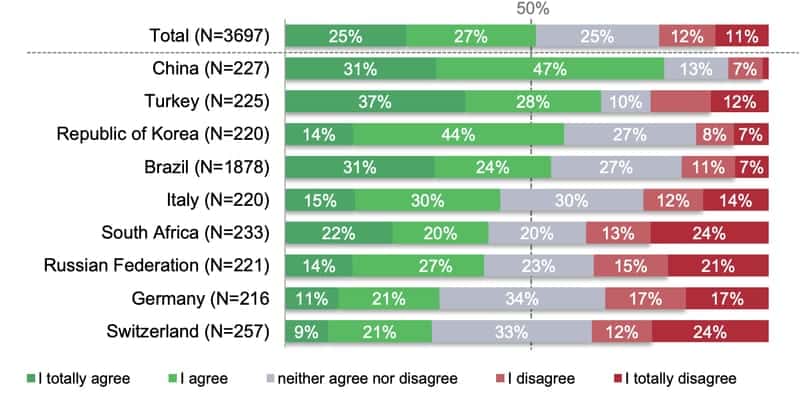

It therefore comes as no surprise that developing countries have shown the biggest relative jump into E-commerce as a result of Covid-19. LATAM and Africa (mainland) have been traditionally relying heavily on cash-payments and were left perplexed in light of the changing landscape. This fact pressed the need to act, and act fast. This phenomenon is also reflected in a survey conducted by the UNCTAD and its results are outlined below (respondents were requested to answer the question Since the outbreak of COVID-19, I am shopping more often online than before):

The need for Online payment solutions

The urgency to move a business online, whether they already have some online presence or not, requires adaptations, compliance with regulations, and the ability to perfect the customer experience and flow.

Many businesses are dumbfounded when they first need to set up a new payment infrastructure, considering that the process of accepting payments is not a plug-and-play solution. The purpose of gateways and orchestration solutions - like ZOOZ - can assist with the need to accept payments and build an infrastructure suitable for a sphere pushed so quickly into E-commerce.

A gateway helps businesses to build a stable, fortified, and flexible ground to build up from—whether they are new to the payment world or are already seasoned actors. Some solutions, like ZOOZ’s PaymentsOS, have make businesses’ lives easier by allowing them to easily add providers, A/B test them, set routing rules for optimization, and more.

Building from scratch or stepping up your game

We see a general division into two types of business-models which evolved as a result of the pandemic —the first are businesses that have already had a payment infrastructure of sorts in place, and the new reality just limelighted their need to expand and scale up their operation; and the second type is businesses new to the payment sphere, which now need to build their infrastructure from scratch. In either case, both models find themselves in need of making changes and adapting; and both can -and should- benefit from the orchestration abilities of gateway-solutions.

Moving forward

As the ripples of Covid-19 continue to hit every aspects of daily living, the payment ecosystem adequately evolves and adapts itself to cater new consumer preferences -both in the demand for certain commodities, and in their preferred methods of payment.

Either way, the linear increase of E-commerce is unlikely to cease in the near future, and we can expect to see a continuous global increase in its use on the expanse of the once popular in-store purchases. We can also expect to see the gap between developing and developed economies continuously decrease in the use of online payments.

Subsequently, the use of payment gateways, solutions, and supporting technologies also expand and grow, and businesses can benefit tremendously from strategically building their payment stack to support their current business needs, while also having in mind the post Covid-19 business reality, which has yet to unfold.

What’s New? At ZOOZ, we continuously strive to improve our products and enhance our offerings. The key is flexibility, variability, and optimization— and these three components go hand in hand to perfect payment stacks and optimize their performance. Here’s a…

January 2021 marked the beginning of a new year and the official implementation of 3DS 2 guidelines for online transactions in Europe (the UK is due on 17 September 2021). 3DS 2 sparks concerns in merchants and providers alike. As…

To combat credit card fraud and protect consumers, card brands like MasterCard, Visa, American Express, Discover and JCB established the PCI Security Standards Council which mandates a set of security standards for managing online payments. What is PCI DSS?…

A well-designed payment stack is made to generate more money for your business. Who wouldn’t want that? But as it turns out, this concept is a bit more complex to implement in practice. As we’ve covered in recent articles, choosing a…

While COVID-19 has hit many sectors hard, e-commerce is one industry where business has boomed. With quarantines and social distancing limiting people’s ability to maintain their purchasing and spending habits in the physical world, consumers are forced to shop online….

Without noticing, COVID-19 has sped up the shift the entire payment ecosystem has been expecting for years— only instead of a slow and gradual transition, many sectors were forced to condense an otherwise year-long process into just a couple of…

Payment orchestration platforms have become the go-to solutions for businesses looking to optimize their payment performance. The following tips show how you can utilize ZOOZ’s unique solution-features to optimize the way you extract information, find payments, or make alterations to,…

7 Tips to make the most out of your payment stack

By Dana Kemper, November 2, 2020

Payment orchestration platforms have become the go-to solutions for businesses looking to optimize their payment performance. The following tips show how you can utilize ZOOZ's unique solution-features to optimize the way you extract information, find payments, or make alterations to, or within your stack— easily. The small tweaks and changes affect transaction approval rates, and should therefore be added to your arsenal for ongoing payment optimization and ease of operation.

Webhooks

Webhooks are designed to alert and give you updates about your stack, but webhooks can be used for more than mere updates. They can also be integrated into your invoicing system, for example, to make the lifecycle of payments more streamlined. Learn more about webhooks here.

Payment Search

Inspecting specific payments in your system is sometimes necessary, and thanks to the ZOOZ elastic search options, payment professionals can easily narrow down payments by using the ready-made design fields or by specific search shortcuts e.g. “amount:123” to find payments according to specific identifications or search with an asterisk (*) to find payments with partial email addresses, reconciliation ID, order ID and more (e.g., “123*” to find “12345”).

Reporting Tools

Reports can be created as complex or as simple as you wish, but it’s important to be aware that there are always to extract more information from your reports and make them richer and more valuable for your BI. Adding additional fields to your reports can give you a better view of your payment’s performance whether you wish to know your provider performance, payment method used, or performance according to geographical location. All of these components add up and affect your approval rates, and should therefore be taken into account in the larger scheme of your payment operation.

Decision Engine

After extracting insights from your payments thanks to the aforementioned reporting tools, the next step is to implement these insights into your actual payment performance. To do that, you have the ZOOZ decision engine. With more than 150 different configurations, every business need can be met with ease. Configurations can be based on card issuing country, target-provider, and even the time of day in which the transaction took place. Open a free demo account today to try the routing engine by yourself!

Instant Retry

Save up to 10% of failed transactions! The Instant Retry feature, a unique ZOOZ ability, allows you to process failed transactions with a backup payment provider, to significantly increase the rate of successful transactions.

Block Payments

Occasionally you may need to avoid undesired or harmful financial traffic by setting pre-defined conditions to block payments. The ZOOZ platform allows you to easily do so via the Decision Engine -> Block Rules feature. Transactions can blocked according to specific transaction-indicators, card properties, transaction amount, or other customized features.

A/B Testing

Optimization starts with the flexibility to route payments. The ZOOZ decision engine allows easy payment routing that's powerful, simple and intuitive interface that allows you to A/B test your providers' performance, assessing where they perform best, and route them optimally. Making changes is easy, and our businesses track and adjust their routing configuration as much as they wish, and even several times a day, as their performance is impacted immediately

For additional tips and tricks, you can always consult our support knowledge-base for frequently asked questions, tools and hacks to make the most of your payments. Check it out here.

What’s New? At ZOOZ, we continuously strive to improve our products and enhance our offerings. The key is flexibility, variability, and optimization— and these three components go hand in hand to perfect payment stacks and optimize their performance. Here’s a…

January 2021 marked the beginning of a new year and the official implementation of 3DS 2 guidelines for online transactions in Europe (the UK is due on 17 September 2021). 3DS 2 sparks concerns in merchants and providers alike. As…

To combat credit card fraud and protect consumers, card brands like MasterCard, Visa, American Express, Discover and JCB established the PCI Security Standards Council which mandates a set of security standards for managing online payments. What is PCI DSS?…

A well-designed payment stack is made to generate more money for your business. Who wouldn’t want that? But as it turns out, this concept is a bit more complex to implement in practice. As we’ve covered in recent articles, choosing a…

While COVID-19 has hit many sectors hard, e-commerce is one industry where business has boomed. With quarantines and social distancing limiting people’s ability to maintain their purchasing and spending habits in the physical world, consumers are forced to shop online….

Without noticing, COVID-19 has sped up the shift the entire payment ecosystem has been expecting for years— only instead of a slow and gradual transition, many sectors were forced to condense an otherwise year-long process into just a couple of…

Payment orchestration platforms have become the go-to solutions for businesses looking to optimize their payment performance. The following tips show how you can utilize ZOOZ’s unique solution-features to optimize the way you extract information, find payments, or make alterations to,…

SCA (strong customer authentication) is fast approaching

By Dana Kemper, September 9, 2020

SCA requirements are scheduled to go into full effect on 14 September 2019. Following the recent document published by the European Banking Authority, many European countries have published respective statements that they will allow an extended time frame to enable payment facilitators to fully comply with regulations. The extension is mostly valid for eCommerce and card payments. Here is a breakdown of the different European countries and their statements:

Austria

Austria announced a temporary enforcement extension for Austrian cards. The enforcement should go into full effect by the end of September.

Belgium

The Belgian regulator released a formal announcement setting out the Bank's expectations regarding the regulatory technical standard for SCA of online payments.

No set timeline has been published as of now.

Denmark

Denmark released an official announcement of an 18 month extension period for SCA . The FSA emphasized that the implementation period will not change the fact that the rules on strong customer authentication will enter into force on 14 September 2019.

Finland

Finland announced a temporary enforcement extension for Finnish cards. The Financial Supervisory Authority will decide on the length of the transitional period this year after further consulting with the supervisors of other Member States.

France

The French are also working on a phased implementation plan, and have released an official document breaking down their current status and plans ahead.

Germany

Payment service providers based in Germany are allowed to make credit card payments on the Internet from September 14, 2019 initially without strong customer authentication. BaFin estimates that the card-issuing payment service providers in Germany are prepared for the new requirements, while companies that use credit card payments on the internet as payees might not be fully prepared yet.

Ireland

Ireland released an announcement stating a migration period limited only to eCommerce transactions. Therefore no disruption to payments systems is anticipated.

Italy

The Italian regulators also released an announcement stating a transitional migration period, although its length of delay has not yet been officially confirmed.

Luxembourg

The Luxembourg regulator announced a temporary enforcement extension for Luxembourg cards. The financial institutions that wish to make use of the extension period are required to inform the CSSF and back their request with a proper migration plan and timelines.

The Netherlands

The DNB (De Nederlandsche Bank) has released the regulator's intention to allow parties that were unable to prepare for SCA (for credit card transactions) a limited extension time - the amount of time hasn't been stated.

Norway

The Norwegian regulator also announced a temporary enforcement extension for eCommerce and card payments. The payment service providers who need to extend their deadline are requested to contact the Financial Supervisory Authority.

Poland

The Polish regulator also announced an extension for Polish cards, contactless payments, and eCommerce. A proper migration plan will need to be submitted by the relevant parties in order to benefit.

Slovenia

Since the authentication of the majority of card payments made in online stores in Slovenia (and the wider EU) is currently protected only by a one-time password received via a text message, such method of authentication does not meet the requirements of SCA. To ensure compliance, the Bank of Slovenia allows an extension for Slovenian payment providers with registered office in Slovenia beyond the deadline of 14 September.

Sweden

The Swedish regulator also published an announcement that allows extension beyond 14 September for SCA. The extension applies for eCommerce transactions made with card payment. A submission of a detailed plan will have to be submitted and should include the company's planned communication activities to inform e-merchants and payment service users about the new conditions.

UK

On 13 August 2019, the UK regulator announced an 18 month phase-in period for SCA requirements on online card payments. As a result, we don't expect banks to fully require SCA for online payments from UK cards until March 2021.

So what should you do as a merchant?

The enforcement of SCA in Europe is treated with great importance so we recommend all merchants to make all necessary arrangement to be compliant on time (i.e. 14 September 2019).

Here at ZOOZ we are following the changes and announcement closely to keep you up-to-date with all of the changes as well as to ensure our merchants' full compliance.

What’s New? At ZOOZ, we continuously strive to improve our products and enhance our offerings. The key is flexibility, variability, and optimization— and these three components go hand in hand to perfect payment stacks and optimize their performance. Here’s a…

January 2021 marked the beginning of a new year and the official implementation of 3DS 2 guidelines for online transactions in Europe (the UK is due on 17 September 2021). 3DS 2 sparks concerns in merchants and providers alike. As…

To combat credit card fraud and protect consumers, card brands like MasterCard, Visa, American Express, Discover and JCB established the PCI Security Standards Council which mandates a set of security standards for managing online payments. What is PCI DSS?…

A well-designed payment stack is made to generate more money for your business. Who wouldn’t want that? But as it turns out, this concept is a bit more complex to implement in practice. As we’ve covered in recent articles, choosing a…

While COVID-19 has hit many sectors hard, e-commerce is one industry where business has boomed. With quarantines and social distancing limiting people’s ability to maintain their purchasing and spending habits in the physical world, consumers are forced to shop online….

Without noticing, COVID-19 has sped up the shift the entire payment ecosystem has been expecting for years— only instead of a slow and gradual transition, many sectors were forced to condense an otherwise year-long process into just a couple of…

Payment orchestration platforms have become the go-to solutions for businesses looking to optimize their payment performance. The following tips show how you can utilize ZOOZ’s unique solution-features to optimize the way you extract information, find payments, or make alterations to,…

3D Secure 2 is coming your way— ensure your compliance

By Dana Kemper, September 4, 2020

The proliferation of mobile technologies and alternative payment channels has made it easier for consumers to make online purchases and led to the rapid growth of e-commerce. But while digital commerce continues to gain in popularity, incidents of fraud are on the rise as the verification of customer identity in card not present transactions becomes a real challenge.

Starting in September 2019, the latest Payment Service Directive, also known as PSD2 will introduce new requirements and begin enforcement of Strong Customer Authentication (SCA) standards for online payments to combat. The 3D Secure 2 messaging protocol will be the preeminent method to help you comply with PSD2- SCA requirements. In this basics guide, we’ll explain what 3D Secure 2 is, its benefits, and help you understand what you’ll need to do to get your operations 3D secure 2 compliant. What is Strong Customer Authentication (SCA) under PSD2? In 2015, the first Payment Services Directive (PSD1) was introduced to regulate payment services and providers throughout the European Union and European Economic Area. Since then, rapid changes in the payments sector have led the EU to upgrade the first Payment Services Directive. The Second Payment Services Directive (PSD2) includes several articles and mandates, one of which focuses on Strong Customer Authentication (SCA). SCA stipulates that two-factor authentication will be required for all electronic payments, with exemptions possible for certain transactions. SCA requires the use of at least two of the following three elements:

Up until now, additional security steps, aka two-factor authentication, have only been a requirement for transactions considered high risk. To accept transactions after SCA gets introduced in Europe in September 2019, merchants with sales to European consumers will need to upgrade their authentication capabilities to allow for two-factor authentication or face declines. In other words, two-factor authentication is going to become the default for all customer-initiated transactions within Europe, unless an exemption applies.

Moving from 3DS 1.0 to 3DS 2.0 EMV Three Domain Secure also known by merchants as 3DS 2 is an authentication tool or protocol introduced by EMVCo and major card brands to help consumers authenticate their identity when making card-not-present transactions by providing an additional security layer. You’ll already be familiar with 3D Secure 1.0 (3DS 1.0) which shared data among critical stakeholders in the payments ecosystem to authenticate transactions. 3D Secure 2 is the updated version of this authentication protocol, which provides improvements that take into consideration SCA regulatory requirements from the European Union, the need to support new payment channels like digital wallets, and declining conversion rates. With 3DS 2 merchants will be able to integrate an additional security layer into their checkout processes which will help them comply with new SCA regulations and fight fraud more effectively without sacrificing the customer experience. Whereas the flow of 3DS 1.0 focused mainly on a simple challenge (insertion of a code on a static webpage, SMS authentication etc.), 3DS 2 facilitates rich data exchange between merchants, card-holders and issuers, more so than ever before to achieve more accurate authentication. Transactions can be verified by merchants using the customer’s issuing bank instead of a customer needing to remember a PIN or getting redirected to a new webpage. The result is a more frictionless payment experience, although in some cases a challenge may be required to verify user identity. Check out the two flows below to get a better understanding of the process:

Rules have exemptions, and 3DS 2 is no different Some transactions will be exempted from the 3DS 2 protocol. These cases may include: - Whitelisted Merchants (or trusted beneficiaries) - Customers will have the opportunity to whitelist any merchant that they deem trustworthy after an initial authentication has occurred. By doing so, most future authentication steps will no longer be required. - Mail order and telephone orders - Card data that is collected from customers over the telephone. - Low-value transactions - Transactions that total less than 30 Euros each, with no more than five transactions allowed in a row. If the total amount on a single card is higher than 100 EUR in 24 hours, SCA will be required. - Low-risk transactions - A transaction is to be considered low risk if it passes an acquirer’s real-time risk assessment and is approved by an issuer on a case-by-case basis. - Recurring transactions/ subscriptions - A subscription-based service that features recurring payments of the same/different value. However, a customer’s first payment will still require authentication.

6 benefits 3DS 2 brings to merchants Harnessing 3DS 2 delivers several benefits for merchants. These include:

1. 3DS 2 helps comply with new SCA mandates which stipulate two-factor authentication as a requirement for all electronic payments. If you have a large number of customers in Europe, employing 3DS 2.0 is a necessity to continue operating. 2. 3DS 2 protects operations with robust security, and has the potential to fight cases of fraud. 3. 3DS 2 provides a great customer experience. Frictionless customer identification has the potential to contribute to a shortened check-out process and to reduce cart abandonment. 4. 3DS 2 increases authorization rates as authentication is quick and can take place on the same page. 5. 3DS 2 allows to easily build authentication flows natively into Apps or websites. 6. 3DS 2 helps to shift liability away from the merchant (the issuing bank assumes the risk).

3DS 2 will have a profound effect on the entire payment ecosystem. ZOOZ is working hard to enable its customers to comply with these regulations in the quickest and most streamlined-way possible. Further information on how ZOOZ is preparing itself for 3DS 2 can be found here.

We hope that the information provided above helps to shed some light and to demystify the fears revolving 3DS 2.0. Want to learn more? stay tuned for more articles coming up in this series by signing up to our newsletter below:

What’s New? At ZOOZ, we continuously strive to improve our products and enhance our offerings. The key is flexibility, variability, and optimization— and these three components go hand in hand to perfect payment stacks and optimize their performance. Here’s a…

January 2021 marked the beginning of a new year and the official implementation of 3DS 2 guidelines for online transactions in Europe (the UK is due on 17 September 2021). 3DS 2 sparks concerns in merchants and providers alike. As…

To combat credit card fraud and protect consumers, card brands like MasterCard, Visa, American Express, Discover and JCB established the PCI Security Standards Council which mandates a set of security standards for managing online payments. What is PCI DSS?…

A well-designed payment stack is made to generate more money for your business. Who wouldn’t want that? But as it turns out, this concept is a bit more complex to implement in practice. As we’ve covered in recent articles, choosing a…

While COVID-19 has hit many sectors hard, e-commerce is one industry where business has boomed. With quarantines and social distancing limiting people’s ability to maintain their purchasing and spending habits in the physical world, consumers are forced to shop online….

Without noticing, COVID-19 has sped up the shift the entire payment ecosystem has been expecting for years— only instead of a slow and gradual transition, many sectors were forced to condense an otherwise year-long process into just a couple of…

Payment orchestration platforms have become the go-to solutions for businesses looking to optimize their payment performance. The following tips show how you can utilize ZOOZ’s unique solution-features to optimize the way you extract information, find payments, or make alterations to,…

Enterprise Payment Hubs: A Key to Hypergrowth Success

By Dana Kemper, August 29, 2020

What are Enterprise Payment Hubs?

Enterprise Payment hubs are becoming a popular solution for e-commerce merchants seeking to combat growing fragmentation and complexity in today’s payments ecosystem. A payment hub, also referred to as a payment orchestration layer or enterprise payments architecture, is a flexible and consolidated platform that manages and controls payment operations end-to-end. Under the hood, a payment hub features all the automation software systems and services that coordinate and manage the activities involved in authorizing, processing, and optimizing payments.

The great thing about a payments hub is that it consolidates lots of different payment-related activities into one place and enables integration with multiple systems and channels. With the right payments hub, merchants have the opportunity to build a smarter, customized and best-in-class payments architecture that can ease payment management, support global growth, and drive efficiencies with advanced optimization in today’s more global, complex, and fragmented payments ecosystem.

Key Features of an Enterprise Payment Hub

A new way to manage your payments

Built for a time when e-commerce was far less complicated, today’s fragmented payment stacks, designed with a segmented siloed approach, are getting harder to manage and fast reaching a breaking point.

After years of getting loaded up with different functionalities, components, and elements, payment stacks have turned into a patchwork of tangled and interlinked software systems that are more of a liability than an asset.

Fragmented payment infrastructures are turning simple payment-related tasks like reconciling deposits into time-consuming and error-prone processes. Straight forward activities involved in a request for a refund are now becoming more difficult.

It can be a real struggle to establish where an original transaction was processed as there are several records to search. Maintenance has become complicated and grown into a continuous drain on resources as well, as has the integration of new providers and payment methods.

Enterprises and hypergrowth merchants need to keep up with a market which is becoming more segmented and diverse by the minute, thus the need for a centralized platform to manage it all becomes paramount. Thanks to their ability to consolidate everything into one system, today's payment hubs give merchant the ease of managing their payments more efficiently and easier than ever before.

Rapid integrations that support global growth

Continuously adding new providers and payment methods is a necessity for hyper-growth merchants branching into new markets, even though fragmented payment infrastructures make extending your payment network far more complicated than it needs to be. Payment hubs, with an emphasis on open payment platforms, enable connectivity to multiple payment providers by easy integration via a single API.

ZOOZ’s payment hub, for instance, provides an agnostic payment infrastructure that removes the cumbersome, inefficiencyand costly processes associated with provider integration. With ZOOZ, merchants are able to integrate and manage new providers quickly and easily via one API, with minimal effort on their side - something which is normally a real pain for merchants.

Advanced payment optimization tools to boost profits

With an ever-increasing number of providers and growing global transaction volumes, it’s essential to have a way to control your exposure to provider declined transactions, which leads to lost sales. It’s also critical to have the ability to optimize transaction flows to avoid expensive fees that take a chunk out of profits.